“Power Tools for Family Finances,” Ensign, June 2009, 34–35

Power Tools for Family Finances

Use them to demolish debt and build a strong financial future.

The First Presidency has counseled: “Pay off debt as quickly as you can, and free yourselves from this bondage” (All Is Safely Gathered In: Family Finances, 2). But how do you do that when your financial house is shaky and you seem to spend all your time and energy just trying to hold it together?

Here’s how one couple might tackle the challenge using some simple but powerful tools available to everyone. “Ruth” and “Elliot” are a composite of many real couples who have used these tools successfully. They have a mortgage balance of $223,345, credit card and retail store debt totaling $8,456, and an $11,465 car loan. They currently spend $25,836 per year on debt payments. Paying off their debts at the current rate will take 25 years. Tired of the strain of juggling bills and feeling no control over their situation, they turn to their bishop, who suggests they visit www.providentliving.org.

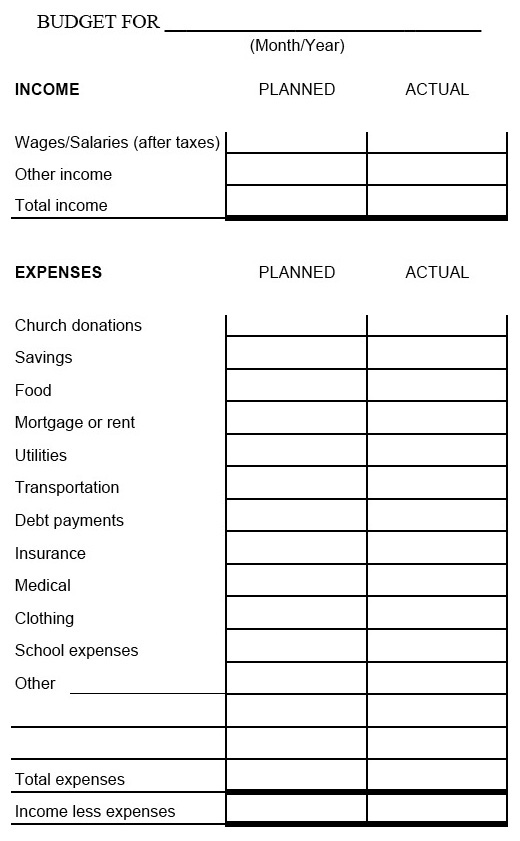

First, Ruth and Elliot use the chart on page 7 of One for the Money (see fig. 1) to create a family budget. In the process, they see expenses that could be eliminated, such as the money Elliot spends each day on soft drinks and snacks at work. They quickly identify $100 per month that could be better spent.

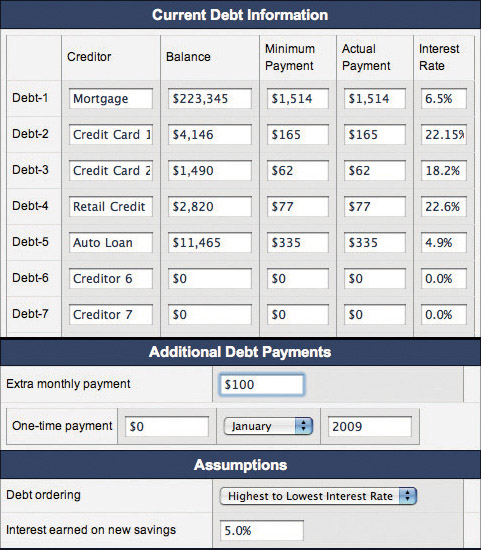

Next, they enter current debt information into the How Soon Could I Pay off All My Debts? calculator (see fig. 2). It shows how funds that are freed up when one debt is repaid can be used to pay down remaining debt. The results are dramatic. Without paying one dollar more per month, they could pay off all their debts in 15 years, 10 years sooner than they would have otherwise (assuming their income remains stable and they incur no additional debt).

Using the same calculator, they now add that $100 per month of misspent money as an extra monthly payment. The result: they will be able to pay off all debt (mortgage included) in just under 14 years. This cuts an additional year off their payoff time. They would save 11 years of payments and $209,392 in interest.

Now Ruth and Elliot wonder: When they no longer have debt payments to make, what would happen if they put the equivalent into savings and added that $1,200 per year of misspent money? To find out, they use the How Much Could I Have If I Saved Regularly? calculator (see fig. 3). Here they enter savings goals based on reasonable assumptions.

What they find both shocks and motivates them. They realize that they will not only save 11 years of debt repayment and $209,392 in interest paid, but could have $429,060 in the bank at the end of the originally scheduled 25-year repayment plan.

Ruth and Elliot may be fictitious, but their situation is reality for many. Details will differ. Some people earn more money, some earn less. Some owe much more money, some people owe much less. No matter. These concepts and tools have universal application.

Photography by David Stoker